Section 24 Tax Changes

Residential Landlords have been on a roller coaster ride, with the SDLT premium of 3{24e7654783ee36f96230dae09932763c2f1ad5e3241502bcdb11cafbcc0ea81d}, buy to let mortgage service ability and Section 24 Tax Changes. This ride will continue util 2021, when the tax changes will have been fully implemented. Income tax changes affecting residential landlords which were announced by the previous government in the Summer Budget of 2015 , have now come into effect. These changes will have a negative effect on residential landlords maintaining their profit levels.

According to HMRC, under Section 24 tax changes, the tax relief that landlords of residential properties get for finance costs is being restricted to the basic rate of Income Tax. This is being phased in from 6 April 2017 and will be fully in place from 6 April 2020 and will affect:

- UK resident individuals who let residential properties in the UK or overseas

- non-UK resident individual who let residential properties in the UK

- individual who let such properties in partnership

- trustee or beneficiary of trusts liable for Income Tax on the property profits

According to recent figures this means that approximately 8.2 million people in England alone will be affected and over half of UK landlords will be pushed into a higher rate of tax despite their income not having increased.

Until now, landlords have been able to deduct the full cost of their mortgage interest payments on their rental properties before they pay tax. Starting April 2017, mortgage, loan and overdraft interest costs will not be considered in calculating taxable rental income. The changes will be phased in gradually over 4 years, starting from 5th April 2017. By 2020, 100{24e7654783ee36f96230dae09932763c2f1ad5e3241502bcdb11cafbcc0ea81d} of finance costs will be restricted to 20{24e7654783ee36f96230dae09932763c2f1ad5e3241502bcdb11cafbcc0ea81d} tax relief only.

Landlords will no longer be able to deduct all of their finance costs (Finance costs include mortgage interest, interest on loans to buy furnishings and fees incurred when taking out or repaying mortgages or loans and capital repayments of a mortgage or loan) from their property income to arrive at their property profits. They will instead receive a basic rate reduction from their income tax liability for their finance costs.

Order Your personalised Report

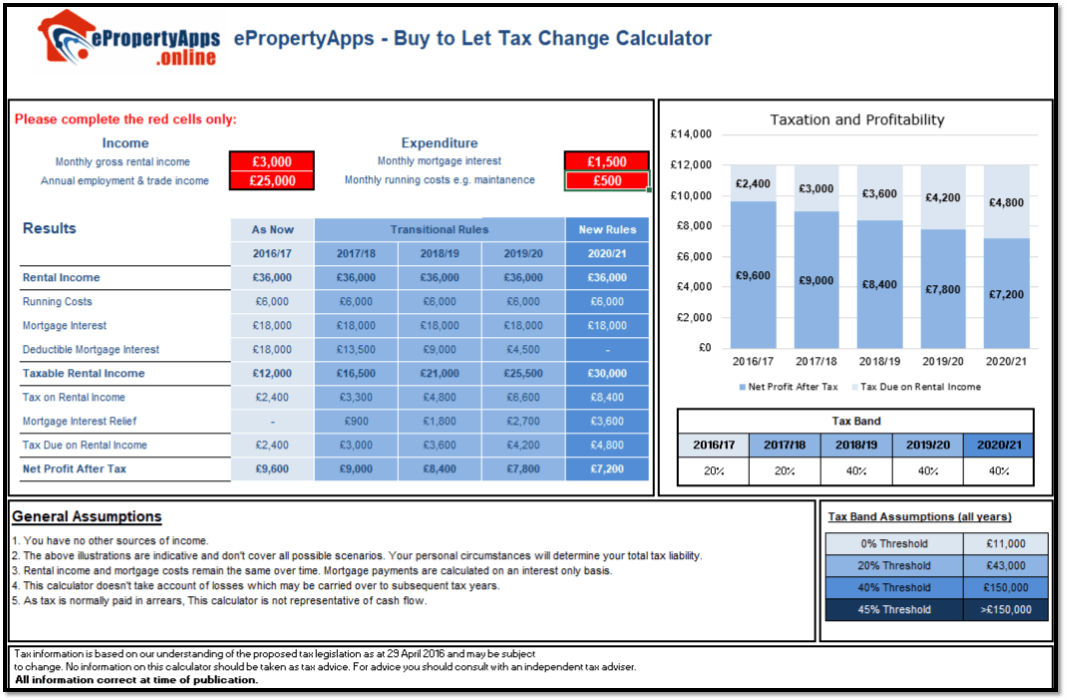

Example:

- An income of £25,000 pa from current employment

- A rental income of £3,000 pcm.

- Monthly finance costs of £1,500

- Monthly running costs of the property of £500

ePropertyApps Section 24 Tax Changes Calculator

The illustration above, from our Tax Changes Calculator, clearly shows the results of the Tax Changes taking effect. Although there is no change in the residential landlord’s income (no increase or decrease) the tax payable in increasing year on year:

- £2,400 in 2016/17

- £3,000 in 2017/18

- £3,600 in 2018/19

- £4,200 in 2019/20

- £4,800 in 2020/21

Additionally, the tax payer has moved into the Higher Rate Tax band (40{24e7654783ee36f96230dae09932763c2f1ad5e3241502bcdb11cafbcc0ea81d}) from year 2018/19.

These reforms mean that the way taxable income is calculated may have other implications for some. For example, if you or your partner receive Child Benefit and your income is over £50,000 the High Income Child Benefit Charge may apply.